The S&P/TSX Capped Telecommunication Service Index outpaces the S&P/TSX Composite Index.

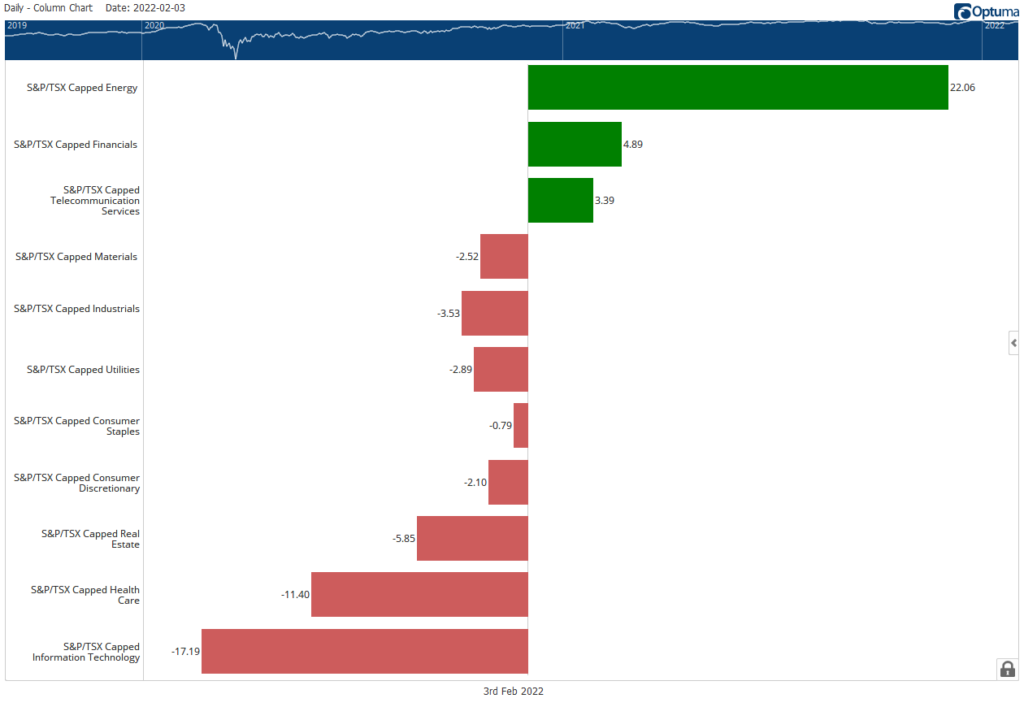

The S&P/TSX Capped Telecommunication Service Index gains membership as a leading sector relative to the S&P/TSX Composite Index. Year to date, Telecommunication Services is up 3.39%, accompanying Financials and Energy which continue to pave the way for Canada’s main index, 4.89% and 22.06% respectively. The broader market is remains in negative territory, down 1.26%, on the backdrop of increasing global market volatility.

The sector index traded above it’s 2020 peaks of $188.05 into a range-bound market for second half of 2021. And, not until recently have we seen price above the index’s high of $199.64, from last September. The upward breakout provided a happy resolution to the choppy ‘tug and pull’ between supply and demand. The breakout is meaningful as it signifies accumulation of overhead supply driven by persistent buying and sector optimism.

Relative strength to the broader market has been expanding since the Q4/2021, highlighted by the relative strength ratio trending above it’s internal upwards sloping exponential moving average, supporting positive price developments.

Momentum has developed into a bullish regime spotlighted by the 14 period relative strength index oscillating in the upper regions of the indicator. Overbought levels in RSI is a positive development for bullish price structures – higher highs in price should be reinforced by sustained demand. Whereas, the lack of would raise caution to recent developments.

As long as price maintains above the $200 level, the sector looks attractive – new highs, expanding relative strength, and price momentum all adding wind to the sails, and to the story.

Telecommunications provide a unique value for long-term investors seeking steady growth and yield.

BCE Inc., Telus Corp., and Rogers Communications Inc. attract attention when discussing the sector due to their market capitalization having greater influence to sector performance. To date, with the exception of Shaw Communications, sector constituents are in positive territories, led by Rogers Communications Inc., up 8.4%. Within the group, it’s BCE Inc. and Telus Corp. that are striding to new highs, closely resembling the sector’s price structure – BCE Inc. and Telus Corp. are up 2.53% and 2.75% respectively. While Rogers Communications Inc. is leading sector performance, price is advancing to a level of resistance at $67. Will market participants absorb Roger’s overhead supply at $67? For now, that remains to be seen, but developments should be on watch.

Telecommunications present a unique appeal for long-term investors seeking steady growth and income. Noted earlier, the sector is leading the broader market on new highs. As a bonus, yield for telecomms are also quite attractive. Considering that BCE, Rogers, and Telus pay 5%, 3%, 4.25% respectively – it would seem that investors can have their cake and eat it too?