Canadian equity markets have benefited from rising energy prices, commodities, and global base metals themes.

The S&P/TSX Composite is up 4% year to date. And similarly, the S&P/TSX Small Cap Index and the TSX 60 Index are also positive, 8.50% and 3.8% respectively. 2022 has been friendly to Canada’s resource heavy economy and equity markets are fairing better relative to our US counterparts. Much of the relative performance can be explained by rising energy prices, commodities, and global base metals contributing to the lift in performance in energy and materials – both sectors are up 38.50% and 22%. South of the border indices are in negative territories. But, let’s not forget that the S&P 500 index has a different composition to the S&P TSX Composite. The latter has positively benefited from commodity related themes due to Canada’s resource heavy composition while the former has limited exposure to them, accounting for only 4% and 2.6% of Energy and Basic Materials.

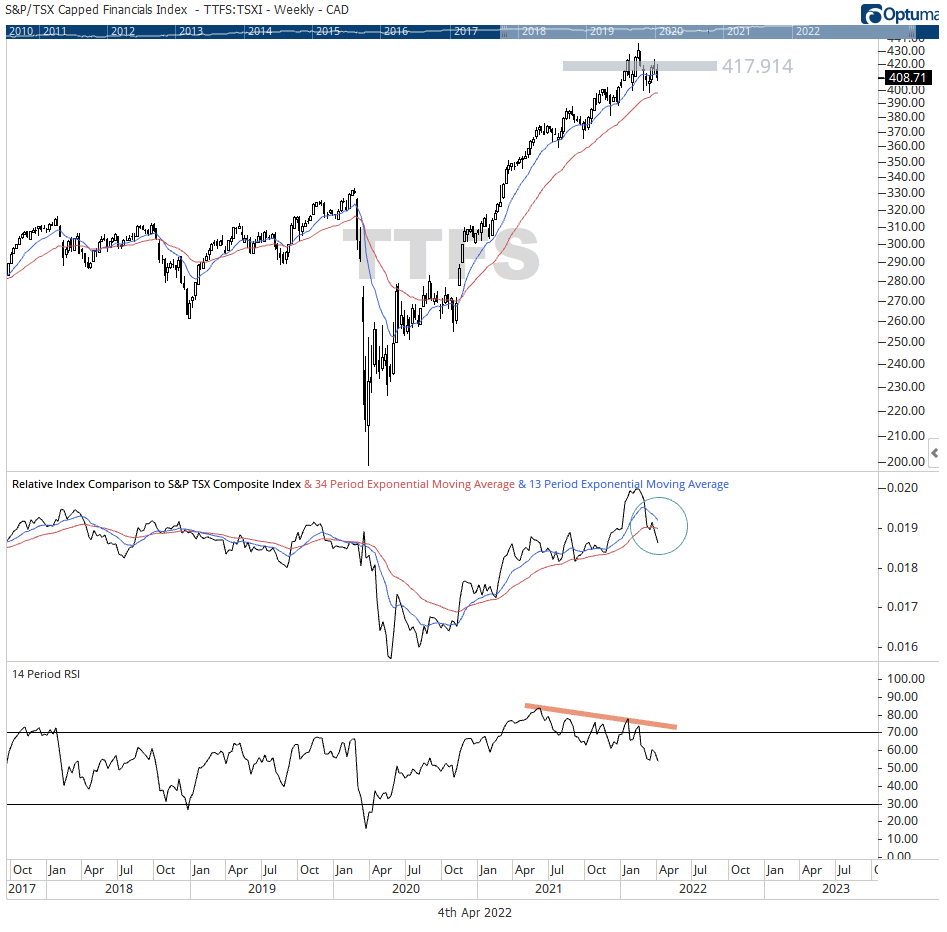

From a longer-term perspective, the S&P TSX Capped Financial Index looks fine, but relative strength and momentum divergence caution for attention.

In an earlier post, the attractiveness of the financials sector was highlighted at the backdrop of rising rates as central banks moved forward to curb rising inflation. While, the financial sector remains in positive territory, 1.40% year to date, the sector’s performance has lagged the broader equity market with the muted sound of Lenny’s “Are You Gonna Go My Way” playing in the background.

Developments in the finance sector has been (and remains) choppy. All the while, the long-term 13/34 weekly model remains positive. From 2020 lows to all time highs, the group ascended by nearly 120%. And naturally, markets do consolidate following a massive rally, providing participants an opportunity for assessment. It’s important to observe that relative strength to the S&P TSX Composite is weakening as the sector undergoes price consolidation. While it’s not a dire event unfolding, it can be challenging to navigate. An upwards resolution would suggest continuance of the trend while a downwards resolution could be a sign of sector distribution. On the weeklies, the trend remains intact – general direction of relative strength is upwards, and price momentum is in a bullish regime. So it would seem that the financials sector looks fine. But, not to be ignored, relative strength and momentum are showing signs of caution and sector exposure should be monitored for signs of further weakness. The group is down 7% from Feb/2022 peaks.

A glance at the dailies brings us closer to the sector’s peaks and troughs and ‘hands on the glass’ look at weakening relative strength. The sector seems to find a support zone around $400. A sustained breakout below this area of support would suggest a sector distribution transitioning to a declining market structure. Relative strength turned negative on the dailies, late Feb/2022, following the sector’s recording of all time highs. Momentum, shown by the 14-period relative strength index, highlights an observable divergence during the price peaks in January and February. While the sector posted new highs in February, it lacked conviction and cautioning near-term headwinds, which in hindsight was a near 10% decline in price. More meaningful is the divergence observed between price and momentum on the weeklies. Often providing a reliable flag to monitor developments ahead to manage sector exposure risk.

An upward resolution of the developing range for the group above $420 (preferably above the all time high) would be a positive and points towards trend continuation. Failing would continue the messy consolidation. A downward resolution would translate to further weakness. From a relative strength perspective, having exposure to a sector that’s not exhibiting market leadership is a difficult long proposition. Sustained breakout below $400 will at the very least provide price direction and clarity. Around $420, the S&P TSX Capped Financial Index finds resistance from overhead supply and entries of long positions in group constituents would prove challenging if that supply is not absorbed by buying pressure.