Global equity markets have been affected, to varying degrees, by the US dollar, tightening monetary policies, and unraveling geopolitics. Both developed and emerging markets have broken-down beneath summer lows to extend market declines.

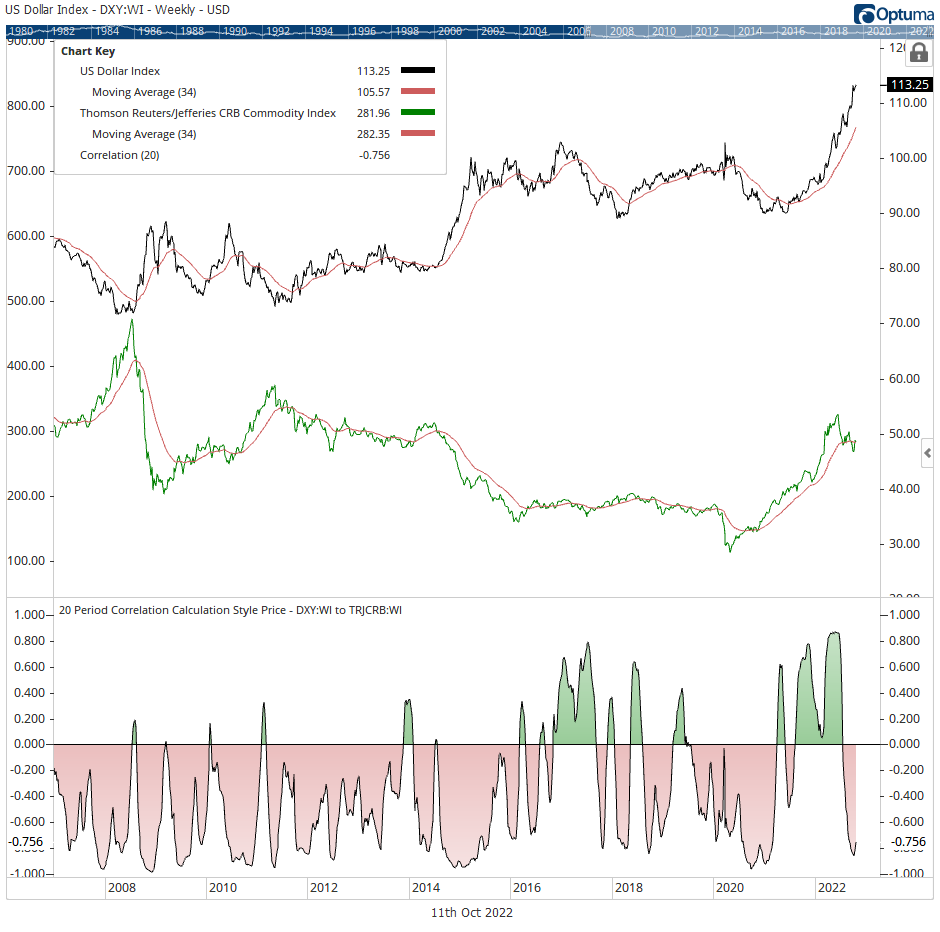

The trend in the US Dollar Index has been robust since its advancement in mid-2021. Year to date, DXY is up 18% and continues to display relative strength against its major economic pairs. The CAD/USD at $0.7256, -8.34% year to date, continues to face headwind on the backdrop of relative strength in the dollar, US economic resilience, rising yields, and recent weakness in oil prices and in the Energy sector. Copper, an industrial metal with wide-spreading economic utility, historically holds a positive correlation to the $CAD – as it does with major exporting economies, such as Canada. Cooper prices are -23.14% year to date and near 2018 levels on weakened global demand.

The Thomson Reuters/Jefferies CRB Commodity Index, despite summer weakness, is up 22% year to date, benefiting from the pandemic supply constraints. Having stepped in tandem with the US Dollar Index for the past year, commodities and the dollar index have reverted to their historically inverted relationship – correlation between the two asset classes is -0.751, a stark contrast to their positive correlation from 2021-2022. Under the hood of the commodities index, crude oil and agricultural markets are showing short-term tailwinds by testing inflection points with their corresponding 34 weekly exponential moving averages. Industrial and precious metals have pulled away from their long-term averages on weakness. Gold at $1,670, has resolved its’ two-year distribution by failing to find support at the absence of buyers in late-September.

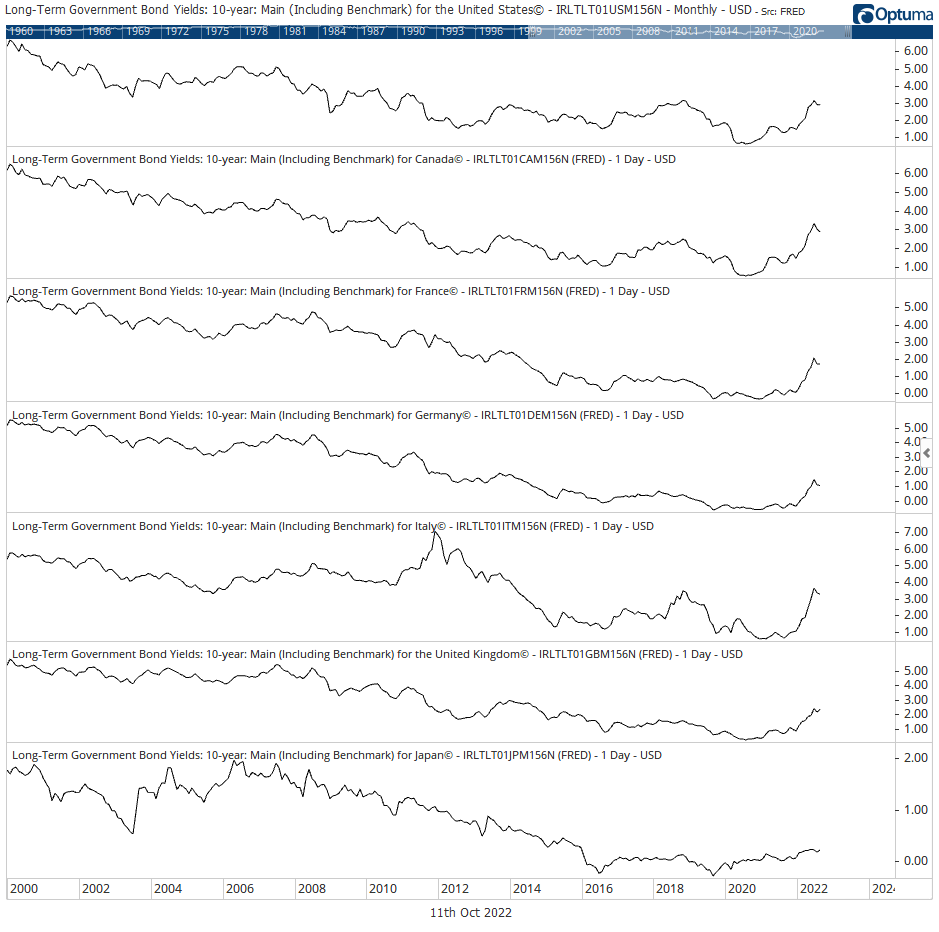

Barring Japan, long-term government bond yields have climbed in harmony as leading economies grapple with inflation. The Japanese 10-year government yield has remained relatively flat, as its’ contemporaries tighten monetary policies. In the US, central bank rate hikes have reverberated through the yield curve resulting in an inversion between the 10- and 2-year treasury yields and a sharp decline in US bond prices. As a proxy for total bond returns, the iShares Core US Aggregate Bond ETF, is -16.43% year to date on bond market volatility. With most asset classes declining in 2022, it’s been an ambitious effort to diversify unsystematic risks.

Global equity markets have been affected, to varying degrees, by the US dollar, tightening monetary policies, and unraveling geopolitics. Both developed and emerging markets have broken-down beneath summer lows to extend market declines. The Dow Jones Industrial Average, a basket of the 30 prominent US companies, declined by 20% from Q1/2022 highs, has been pronounced into the bear market club. From comparable points of reference, the Nasdaq dropped by 36% and the S&P 500 fell by 26%. In Canada, the market picture isn’t much better – the TSX Composite Index, the TSX 60, and the S&P/TSX Small Cap Index have declined by 18%, 18.5%, and 26% from their respective 2022 highs. Relative strength in the Energy group has buoyed Canadian indices above ‘bear market’ proclamation, but how long will it last with Canadian markets checking summer lows. To quote anonymous wisdom, “for prices to rise, they first need to stop falling”, failing to catch a bid will extend the decline and delay recovery. Market breadth for North American indices continue to display a bearish bias – the weekly Advance/Decline Line seemingly continues to deteriorate and percentage of stocks above 200-day SMAs remain sluggish – 90% of constituents are bearish in S&P/TSX Composite Index and 85% are below their 200 SMAs in the S&P 500 on a weekly basis.