By comparison, the US Dollar fell 9.78%, while the Thomson Reuters/Core Commodity Index edged up 0.44%—stifled by a decline in oil prices. Conversely, global equities (MSCI ACWI) surged 19.14%, and US Government Bonds (iShares 7-10 Year Treasury) gained 4.60%.

Gold shined brightly in 2025, hitting all-time highs.

Gold demand stems from four primary sectors: jewelry, technology, central bank reserves, and investment. The latter two have acted as the main catalysts for gold’s 65% year-to-date surge. While the asset spent 2020 through 2024 building a significant base, it is firmly bullish according to the 8/40-week EMA model. However, momentum (MACD) is waning, and capital flow into the asset (MFI) is also diminishing. These divergences from price action suggest that the most recent leg of the advance is lacking conviction, signaling potential exhaustion in the near term.

Global central banks strategically hoard gold for reserves.

Central bank gold buying has reached its highest levels in decades, led by net purchases in Poland, Kazakhstan, Turkey, China, and Brazil. These institutions are accumulating gold as strategic financial insurance, motivated by:

- De-dollarization and Sanctions Risks: Emerging market and European central banks have significantly increased their gold-to-reserve ratios. In August 2025, for the first time since 1996, the total value of global central bank gold reserves surpassed the value of their US Treasury holdings, marking a fundamental regime shift.

- Diversification from US Treasuries: With US national debt reaching historic heights, global central banks have raised concerns regarding the long-term stability of the dollar and are diversifying US exposure strategically.

- Reclassification as a Tier 1 Risk-Free Asset: Under the latest Basel III banking standards, gold is classified as a Tier 1 risk-free asset—banks can use physical gold to meet reserve requirements without the volatility penalty they once faced. Essentially, central and commercial banks are refilling their “Tier 1 buckets” with an asset that cannot be devalued by inflation or frozen by sanctions, treating it with the same regulatory weight as physical cash or government bonds.

- Safe-Haven Status: Gold remains the traditional hedge against inflation and a vital store of value during periods of economic volatility and market uncertainty.

At the end of November, global gold ETF inflows totaled to $77B in 2025, contributing to the pot of US$530B in AUM.

Aggregated data from the World Gold Council highlights that US$5.2 billion flowed globally into physically backed gold ETFs. This aggressive demand was driven primarily by Asia and Europe; meanwhile, North American inflows shrunk notably as investors took profits off the table, following previous months of heavy buying.

- SPDR Gold Shares (est. $147 Billion AUM): As the largest gold-backed ETF, it remains the preferred vehicle for institutional investors due to its deep liquidity and high trading volume. It has recorded significant inflows fueled by gold’s historic rally, persistent economic uncertainty, and heightened geopolitical tensions.

- iShares Gold Trust Micro (est. $5.8 Billion AUM): This fund also saw massive inflows, reflecting a surge in retail investor interest and a preference for lower-cost entry points and lower management fees.

Historically, gold has maintained a high positive correlation coefficient (0.92) with the Canada’s S&P/TSX Capped Materials Index, highlighting that gold prices and Canadian resource equities have a strong tendency to move in the same direction.

Higher gold prices are good for gold miners, and what’s good for gold miners is good for Canada’s Materials sector.

Higher prices provide a strong incentive for miners to increase quantity supplied. These elevated gold prices translate directly into improved cash flows, stronger balance sheets, and increased shareholder returns. Year-to-date, the SPDR Gold Shares (GLD) rose 64.61%, while miners—represented by the VanEck Gold Miners ETF (GDX)—surged by 148.11% over the same period. Miners benefit from rising gold prices through operational leverage—a mining company’s costs (labor, equipment, and fuel) are relatively fixed, a small percentage increase in the price of gold can lead to a disproportionate increase in net profit—making mining equities a highly attractive vehicle for investors during a bullion bull market.

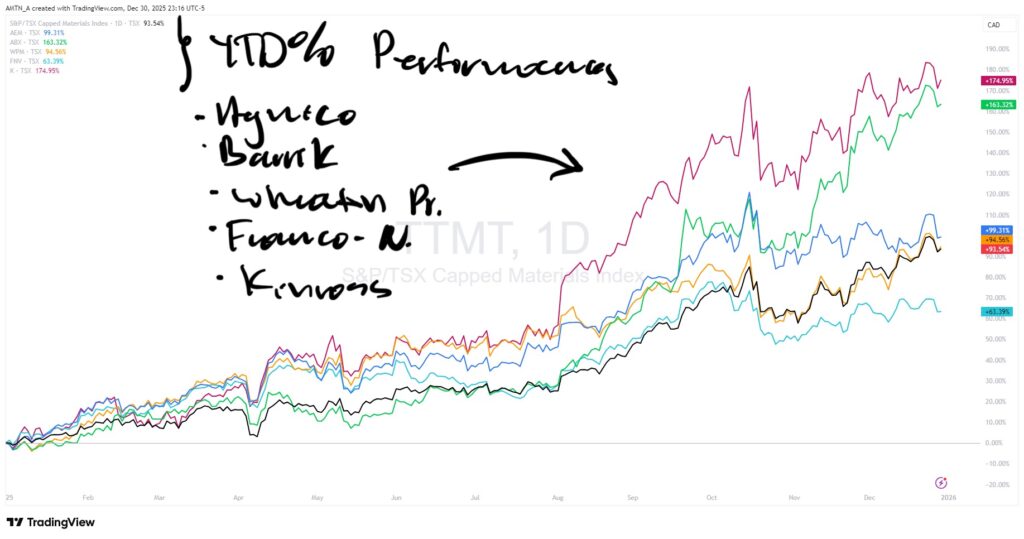

iShares S&P/TSX Capped Materials Index ETF (93.07% YTD) is designed to replicate the performance of the S&P/TSX Capped Materials Index (93.36% YTD). Its sector components are heavily weighted toward gold (73.58%), followed by copper (7.22%), diversified metals and mining (7.17%), fertilizers and agricultural chemicals (5.04%), and silver (3.00%).

Concentrated Exposure: Nearly 50% of the index weighting is accounted for by the top five holdings, which consist of major gold miners and royalty streamers:

- Agnico Eagle Mines Ltd. (14.30%)

- Barrick Gold Corp. (12.34%)

- Wheaton Precious Metals Corp. (8.85%)

- Franco-Nevada Corp. (6.65%)

- Kinross Gold Corp. (5.65%)

Structurally, the index accumulated between 2020 and 2024, finally resolving upwards on the back of rising gold prices. In early November, the sector reverted back to its 8-week EMA before continuing to advance. However, this move occurred alongside slowing momentum (MACD) and diminishing capital inflows (MFI). After briefly testing the October overhead resistance levels, the index advanced further—though the combination of cooling momentum and diminishing money flow suggests a need for caution regarding the sustainability of the current trend.

‘Smart money’ continues to hedge on strong price advance, while non-commercial traders overcrowd the trend.

Commercial Hedgers & Market Sentiment: Commercial hedgers—entities directly involved in the production, processing, or consumption of gold—utilize the futures market to lock in prices for future production.

- The “Smart Money” Proxy: Because their positions are rooted in physical supply and demand, their activities are often viewed as a reflection of the market’s fundamental health.

- Hedging the Rally: During gold’s historic rise in 2025, commercial traders aggressively increased their short positions to hedge against potential price reversals. In late 2024, this net short position reached a net-short position of 345,000 contracts.

- Current Positioning: As of late December 2025, hedgers remain significantly net short of 274.36K contracts. While this is an improvement from the recent extremes, it confirms that producers are still actively selling futures to lock in these historically high prices, providing a potential headwind for further immediate gains.

Large Speculators (Managed Money): This group includes hedge funds, commodity trading advisors (CTAs), and other professional speculators. Unlike commercial hedgers, these participants do not deal in physical gold; their primary goal is to profit from price movements.

- Trend-Following Behavior: Speculators are typically trend followers, accumulating net long positions as gold prices rise. This makes their positioning provides a gauge of market momentum and sentiment extremes.

- Crowded Trade Warning: Large speculators currently hold a net long position of 233.98K contracts. While significant, this has declined from the historic overcrowded extreme of 355.00K contracts seen in early Q1/2020.

- The Reversal Risk: When speculative long positioning reaches extreme highs, it often suggests that “everyone who wants to buy has already bought in.” The lack of new buyers leaves the market vulnerable to a long liquidation event—where selling from speculators can lead to a trend reversal.

While the trend is our friend, the optimism that carried gold to $4,476.56/oz is now met with increasing reservations.

Central Banks as Strategic Anchors: Central banks have been the primary catalysts for gold’s rise. According to the World Gold Council’s 2025 Central Bank Survey, global buying is likely to persist into 2026 as institutions seek a strategic hedge against geopolitical instability. The survey revealed that 95% of central banks expect global gold reserves to increase over the next year. This trend is being led by the likes of Poland (raising its gold reserve target to 30%), China (has a gold-to-reserve ration of 7-10%), India, Turkey, and the Czech Republic, whose policy actions will continue to be a deciding factor in gold’s long-term price development.

Futures Market Sentiment: In the futures market, commercial net-short positions remain near historic extremes. This suggests that smart money producers are continuing to hedge their operational bets, locking in prices at these levels.

The Waning Speculative Edge: Simultaneously, money managers are shrinking their net-long positions. This indicates either a wave of profit-taking or a growing interest in selling futures. Either way, their activity reflects a tapering of conviction among trend-followers.

Risk Management & FOMO: While the weekly trend in gold futures and the S&P/TSX Materials Index remains intact, the persistent divergences in momentum and money flow warrant diligent risk management. For investors experiencing “FOMO”, these signals serve as a strong warning against chasing the market at these levels.

The Bottom Line: These varied vantage points—fundamental, sentimental, and technical—provide a multi-layered perspective. However, this information remains a set of warnings rather than a “sell” signal. The bullish trend technically remains in place until the price structure of gold and the S&P/TSX Materials Index confirm a distribution followed by a decline—supported by a negative 8/40 Weekly EMA.