The US Dollar Index broke out of a seven year consolidation while the CRB Index retreated on persistent dollar strength.

The US Dollar Index, up 12% year to date, continues to display relative strength against the currencies of major US trading partners. The Euro in particular, accounting for approximately 60% of the index has depreciated near parity to the US greenback ($1.01 Euro/USD) on the backdrop of surging natural gas prices in Europe, war between Ukraine and Russia, and global financial market volatility — all contributing to the rise in the dollar. Since 2020, the Commodities Index and the greenback have maintained positive correlation. However, it would seem that they’re resuming their normally inverse relationship. DXY broke out of a seven year consolidation while the CRB retreated on persistent relative strength. Crude oil has fallen by 17.5%, gold is down 4%, and silver declined by 11% in June. Copper prices, a proxy for gauging global economic health, due to its widespread utility, has fallen by nearly 21% during the period. Agricultural commodities such as corn, wheat, coffee, sugar, etc. were also impacted on the dollar strength. The Invesco Agriculture Fund (DBA), for example, invests in various agricultural resources declined by 9% last month. Taking into account rising interest rates and market expectation of slowing economic growth, commodities are certainly feeling stressed as of late.

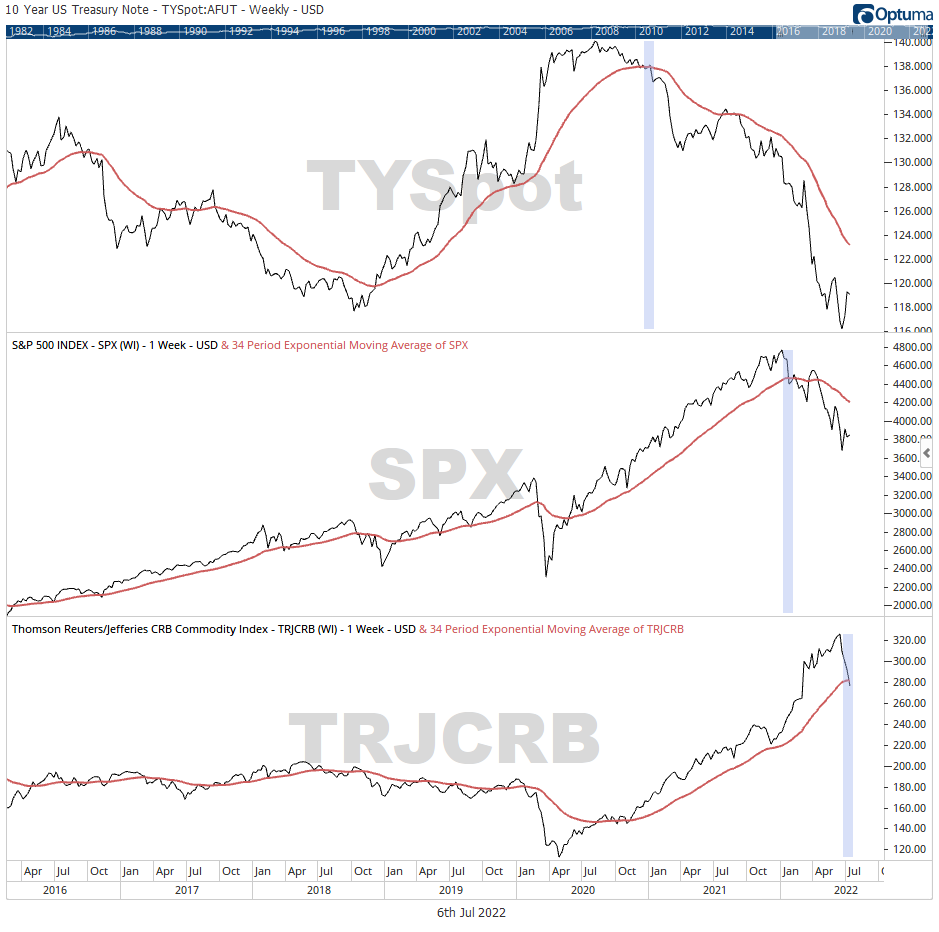

Bond prices and commodity prices generally have an inverse relationship. Surging commodities can lead to an inflationary environment leading to downward pressure in bond prices as tightening monetary polices aim to cool off a potentially overheated economy. The 10 Year Treasury Yield, TNX, is at an important area of 3%, which has been tested more than once in the past 10 years. In 2013, the phasing out of quantitative easing led to a decline in bond prices. And, 2018/2019 was a volatile period — multiple rate hikes, fears of economic growth slowing, and escalating trade conflicts between US and China led to a surge in bonds, and 10 year yields retracted from prior 2013 resistance levels. Interest rates have risen sharply in 2022 — faster than expected, in attempt to combat the fastest pace of inflation in the US in four decades, ascending at an annualized rate of 8.60% in June.

Surging commodities can lead to inflationary pressures leading to downward pressure in bond prices as tightening monetary polices aim to cool off a potentially overheated economy.

Bond yields and bond prices move in opposite directions, and bond prices and stocks generally move in a similar heading, long term. Bond prices tend to peak and trough ahead of stocks, and commodities last — providing valuable market information. The 10 Year Treasuries Yields, a benchmark for the cost of money and yardstick for investor confidence, crossed below its internal 34 weekly EMA in late 2020 on rising interest rates. The S&P 500, barometer for US large-cap equities, peaked at the later half of 2021 and crossed below its 34 EMA as tightening policies cautioned risk-off investor appetite. A persistent rise in the US Dollar tends to weaken commodities, impact exporting transactions, and reduce the value of overseas earnings of multi-national corporations. Bond prices have fallen, equities have fallen, and commodities look to be following, in an orderly fashion? The CRB Index has fallen by 16% from May highs. And, the US Dollar looks to continue playing an influential role ahead.