The US Dollar Index is a basket of currencies representing major US trading partners – the loonie, the euro, Japanese yen, Swiss franc, British pound, and Swedish krona. A rise in the US Dollar Index implies relative strength against these currencies.

Commodities tend to benefit from a relative weakness in the US dollar. Since major commodities are priced in $USD and are globally traded, a decline in the greenback increases the purchasing power of foreign currencies – commodities and the US dollar generally have an inverse relationship to one another.

Throughout 2022, the US Dollar Index shared a similar trajectory to the CRB Commodities Index which counters their generally negative correlation. The value of the $USD can be influenced by a number of factors – currency demand, geopolitics, economic strength, trade balances, monetary policies, etc. Geopolitics, such as war, can bring out uncertainties and drive flight to safety, increasing demand for safe-haven assets. A safe haven asset may provide a store of value during periods of market volatility as investors seek out risk-off options for temporary shelter. As the global market concerns heightened, so did demand for the US dollar.

The US Dollar Index looks to be retreating from 2020/2016 levels and pulling back to an eight year rangebound pattern. The decline is supporting the recent breakout of the CRB Commodities Index from 2014 resistance levels, possibly resuming their inverse relationship. Rising commodity prices is inflationary and coincides with contractionary central bank policies. Generally, rising commodity prices and bond yields trend in the same direction while bond prices and commodities tend to move in opposite direction.

The CRB Index is a proxy for global commodity markets – used to gauge the movement of price for a basket of 19 commodities that includes energy, agriculture, precious metals, and industrial metals.

The Commodities/Bond ratio, like the Commodities Index, has risen and seemingly continues to move upwards indicating relative strength of commodities to bond prices – signaling inflation and higher interest rates. From a portfolio strategy perspective, commodity related stocks continue to remain favorable in periods of high inflation. While relative strength in commodities is a positive to certain markets, higher rates can negatively impact other markets, like stocks.

In the early stages of economic expansion, easing of monetary policies support stimulation of economic activity which results in relative strength in bonds. During the period, equities may still exhibit relative weakness but eventually turn up on growing economic confidence. Bonds and equities move in similar fashion and commodity prices rise on growing demand on the back of strong economic growth. In the later stages of the business cycle, increasing inflationary pressures amount from relative strength in commodities leading to contractionary actions by central banks and downward pressure in bond prices. Central bank rate hikes are eventually priced in the equities market leading to downward pressure in stocks. Increasing costs of capital tends to dampen business investing and simmers economic growth – reducing demand for raw materials and easing inflationary pressures leading to a decline in commodity prices.

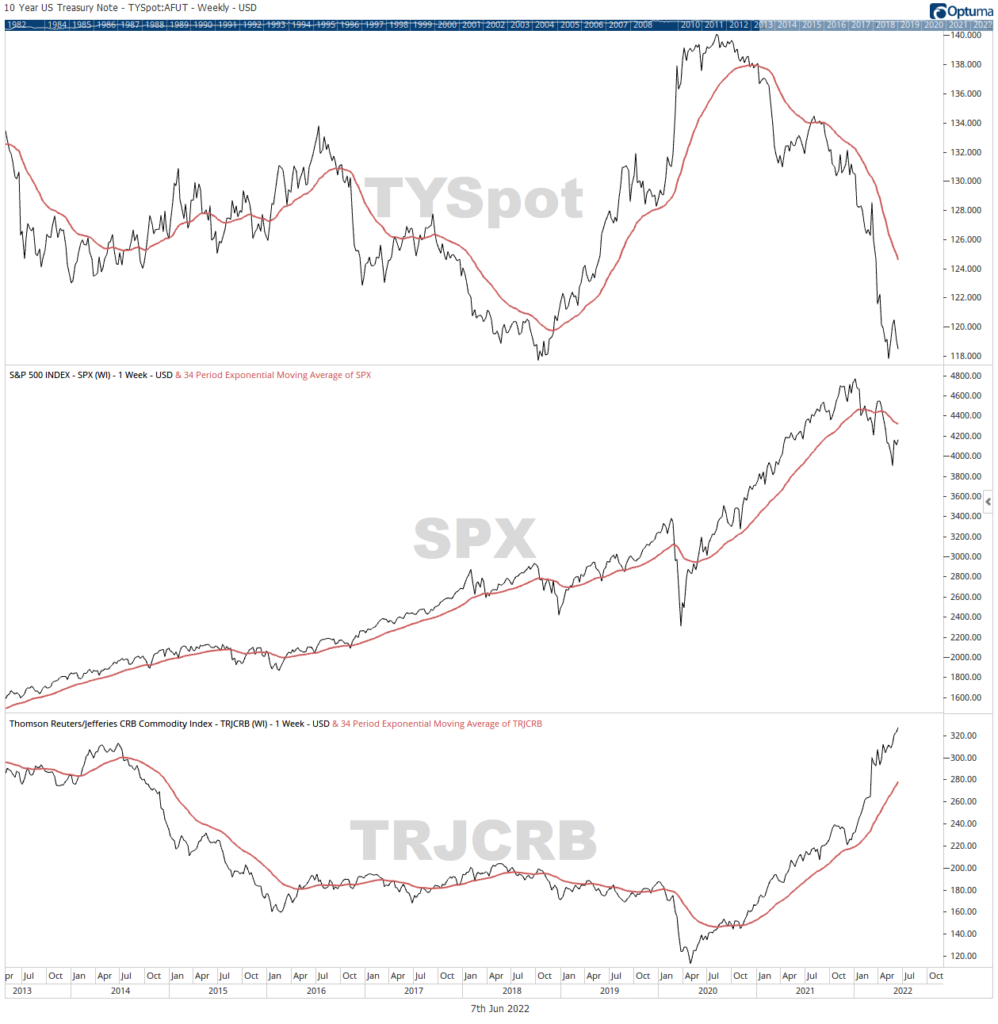

The business cycle has an important relationship with financial markets. The oscillation from economic expansion to economic contraction is filtered across commodities, bonds, and equities. The performance of financial assets are influenced by the phases of the business cycle. As economic expansion reaches maturity, bonds are often first to peak, followed by equities, and commodities are last to turn over. Financial markets don’t always stick to an orderly script, but considering for the intermarket relationships between commodities, bonds, and equities does provide a balanced perspective in assessing the market as the business cycle oscillates.

The continued relative strength in commodities after bond prices and equities have fallen below their respective 34 weekly EMAs, is valuable information – the market is pricing in economic contraction. Year to date, the Thomson Reuters/Jefferies CRB Commodities Index is up 40% and inflation remains front and center. The equities market is likely to be challenged in a continued environment of persistent inflation and rising interest rates. In such an environment, commodities remain attractive until inflation eases and the baton is passed back to bonds.